—

Plan MEDIPARTNER: partnership network (lecture 7/8)

Watch the seventh lecture from 8 lectures course running under the title „Innovation for better healthcare” at University for modern Slovakia. In this lecture, Peter Pažitný and Tomáš Szalay talk about a partnership network, innovation in payment mechanisms and innovative project of managed health care “Plan MEDIPARTNER”, which started in Slovakia in 2012. The lecture video includes English subtitles. Transcript together with the all schemas can be found under the video.

1. What we have learned during the previous 6 lectures?

We have learned that:

- We live in the era of chronic diseases

- Reward based healthcare works

- Three party payments are dominant in healthcare

- In the Netherlands, people may choose among 59 insurance products – insurance plans

- Cash – flow defines behavior

- Innovations in payment mechanisms are important, if we want to improve coordination and results of healthcare

All these claims are being merged in the Plan MEDIPARTNER, the first real health insurance product in Slovakia.

2. About the Plan MEDIPARTNER

Plan MEDIPARTNER:

- The system was developed in the Czech Republic and was operated between 2003 – 2010 by the Metallurgical Employees Insurance Company

- Plan MEDIPARTNER is a strategic vision of the Dôvera Health Insurance Company on differentiating value for consumers on the market

- KlientPRO SK and Dôvera health insurance company launched the Plan MEDIPARTNER in Košice, where administration of the Plan MEDIPARTNER runs since 1 July 2012

- In Košice more than 40.000 insured of the Dôvera health insurance company participate in the plan, out of which 6.000 are active clients of the Plan MEDIPARTNER

3. What is the Plan MEDIPARTNER?

Plan MEDIPARTNER is a modern health insurance product, which integrates the partnership network of healthcare providers with a motivation program for the insured. We will talk about the benefits of the clients in the last lecture. Today we will focus on the partnership network of healthcare providers and innovation in payment mechanisms.

4. What is the network of healthcare providers?

Healthcare providers are not grouped according to ownership, but based on their common interest:

- Voluntary approach – when fulfilling the conditions (in Košice it is 53 general practitioners and 2 hospitals – Hospital Šaca and Železničná Hospital), the entry is possible only once a year, always on 1 July.

- Innovative payment mechanism – full risk capitation – general practitioners and the hospitals are responsible for the overall costs of the insured of the Plan

- Higher quality and coordination of healthcare

- Direction of the demand

- Sharing savings, but also losses

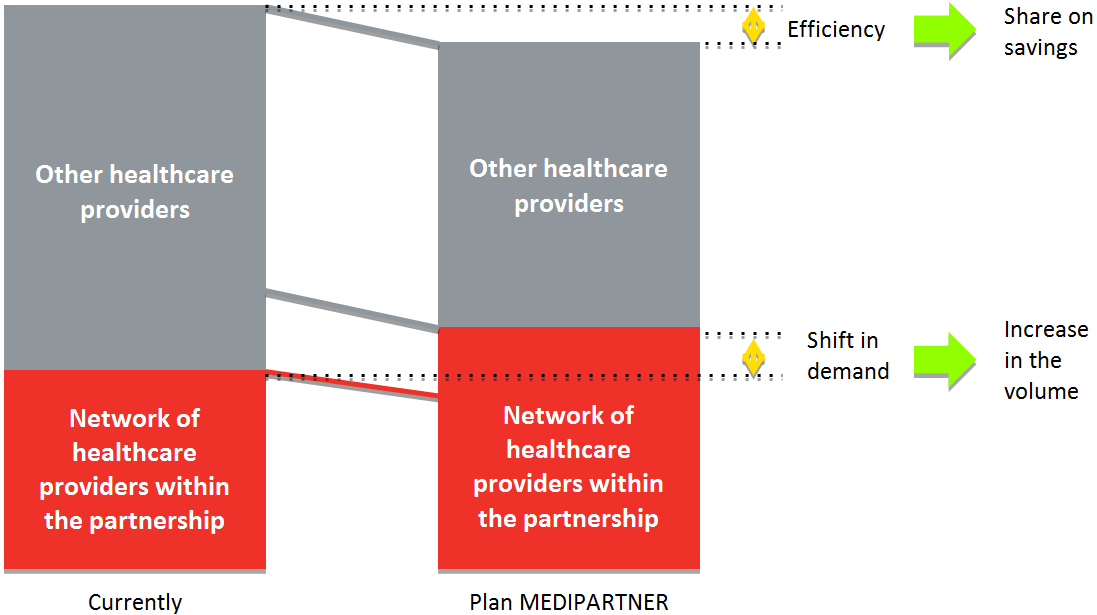

5. How does the principle of demand direction operate in the partnership network?

Partnership network obtains two benefits:

- Increase in the production (for lower unit price) compared to the competitive healthcare providers, which are not in the network

- Share on total savings, which can be established with higher efficiency in service provision (more production for lower price)

Scheme 1: The principle of demand direction of the partnership network

Source: Klient PRO SK and the Dôvera health insurance company

6. What is the demand direction based on?

Demand direction must be beneficial both for healthcare providers within the partnership as well as for the insured:

- provision of quality healthcare

- lower unit costs

- willingness of the healthcare providers in partnership to obtain additional orders

- reasonable indication of further healthcare provided

- better coordination and communication among healthcare providers

7. What is the Plan MEDIPARTNER financed from?

From savings. Savings are being made based on a comparison of costs in the region, i.e. group of insured of the health insurance company Dôvera from Košice and the region, which are not part of the Plan MEDIPARTNER (so called Reference group of insured of the Plan).

That means, savings are not calculated by finding out if the costs of the group of insured of the Plan MEDIPARTNER between the current and the previous quarter were lower, but finding out if the costs in the same quarter for the group of insured in the Plan MEDIPARTNER are lower than of those, who are not members of the Plan.

In order to make this comparison precise, three conditions have to be fulfilled:

- group of insured of the Plan MEDIPARTNER as well as the Reference group of insured have to be evaluated in a very fairly manner (age, gender, economic activity and PCG)

- risk structure of both of the groups of insured is in the beginning compared and the scratch-line is equaled through a so called difference – the line compensates during the whole period the initial differences of the risks of both groups of insured

- from both groups of insured, extreme risks are excluded

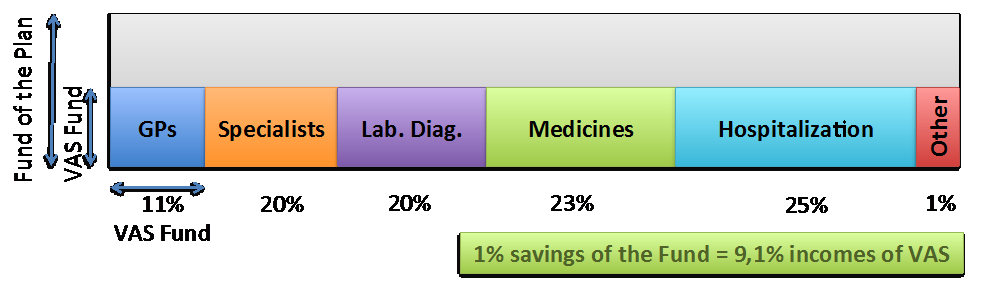

8. How does the full risk capitation work in the Plan MEDIPARTNER?

General practitioners, who are members of the Plan MEDIPARTNER, take over some of the functions of the health insurance company. They take over the responsibility for part of the costs that are meant for healthcare services provided. With other words, they start to bear the risk, which under normal circumstances bears the health insurance company.

Healthcare providers in the Plan MEDIPARTNER are responsible for the costs of the group of the insured of the Plan MEDIPARTNER. The responsibility is divided between two funds:

- VAS Fund – general practitioners are responsible for it

- Fund of the Plan – large healthcare providers are responsible for it (two hospitals)

Scheme 2: The VAS Fund and the Fund of the Plan

Source: Klient PRO SK and Dôvera Health Insurance Company

If they were not participating in the Plan, their income would be dependable from the number of insured in the providers‘ card register multiplied by the monthly capitation unit, disregarding how good or bad are the patients treated or how much they cost the health insurance company.

Costs for the insured are ten times higher than the benefit for the general practitioner. The main idea of the Plan MEDIPARTNER is therefore: to provide doctors the responsibility for the costs on medicines, laboratory treatments, specialists’s visits or hospitalization. And if they manage to achieve some savings – by fulfilling all lega artis procedures, i.e. in compliance with modern clinical knowledge – they receive part of the savings reimbursed as an additional reward to the capitation.

Therefore, general practitioners get a virtual financial fund at their disposal, out of which the treatment of their patients is paid. The amount of the sources in the fund is calculated based on the morbidity of their capitated patients. Doctors with a sicker group of insured have therefore more resources at their disposal than doctors with healthier insured.

9. How does spreading of risk work?

Doctors in the Plan bear the risk for situations, when costs for their group of insured will be for some reason too high. They are protected for such risks by dividing risk among each other, i.e. among more doctors. They create a solidarity group. Based on experiences, if a group of doctors takes care of more than 20.000 insured, accidental fluctuations cannot destabilize costs for these insured for more than 0.5 percent.

General practitioners cannot influence all costs. If they took over the responsibility for all costs, some costs – so called catastrophic, such as a hospitalization of patients after a serious accident at the intensive care unit for one month – could ruin them. Ultimately, the responsibility for catastrophic costs is the responsibility of the health insurance company.

General practitioners in the Plan within the VAS Fund bear only a limited risk – for instance for medicines, which are not bound on a specialist, in case of specialized ambulatory care they only bear the costs for treatments up to 15 € per visit, in case of hospitalization up to 120 € per case and 30 € for each day spent at the hospital. Then a stop-loss situation occurs – additional costs are borne by the Fund of the Plan, in which two hospitals are grouped. If the risks were too high for them as well, it would be taken over by the health insurance company.

10. How does this mechanism work in practice?

Contracted capitation for doctors in the Plan MEDIPARTNER is increased by 30%. However, doctors do not get these 30% reimbursed immediately. This reimbursement is conditioned by achieving savings – whether the group achieves savings is evaluated continuously, but in the accounting it is finalized only once a year.

Until then, resources for this increased capitation are accumulated, which is called in the Plan MEDIPARTNER as withholdings. These resources are stored like in a notary subsidy, detained until the year-end closing.

And so it is even more complicated, the withholdings do not contain only the resources for the additional 30% of capitation, but 35% of the capitation. Thus, the doctor enters the Plan in a way that he/she receives 5% less resources than until now. In the worse situation, doctors in the Plan would receive less than those doctors, who are not part of the Plan. However, the threat of not receiving the 5% of capitation forces him/her to activity.

A similar experience has been discovered in the 70s by two economists Amos Tversky and Daniel Kahneman. They called it „loss aversion“, meaning „fear of loss“. People have a conscious resistance towards losses, which is higher than satisfaction made by profits. The behavioral economist Dan Ariely writes about such and other psychological phenomenon influencing economics in a very interesting way, whose book „Predictably Irrational“, I highly recommend you.

11. What is a saving?

How to find out that doctors achieved savings? By comparing costs for insured capitated for doctors who are members of the Plan and insured capitated for doctors, who are not members of the Plan. The sickness of the insured is of course taken into consideration, so that comparable units are compared. And the important thing is that the reference sample of doctors – those, who are not members of the Plan – is chosen from the same region, so that regional epidemiological specifications are taken into consideration.

If costs for an average insured in the Plan MEDIPARTNER are lower than in the reference group, the group achieved savings and the withholdings are paid to the doctors. Other resources are divided based on merits – i.e. according to, which doctor contributed to the result of the group mostly.

If savings are higher than the amount of withholdings, doctors get a claim for bonus capitation. This makes one third of the additional savings. One third is received by the health insurance company and one third serves for securing costs in the next accounting period of the Plan.

Summary

- Plan MEDIPARTNER is the first real health insurance product in Slovakia

- It integrates a partnership network of healthcare providers and motivation program

- Healthcare providers are not grouped based on ownership, but based on common interest

-

The partnership network obtains two benefits:

- Increase of the production volume

- Share on savings

- Plan MEDIPARTNER is financed from savings

- In the Plan MEDIPARTNER, general practitioners are reimbursed through full risk capitation

-

Sharing the risk works in two ways:

- Costs are calculated for a group of doctors and risks are correctly evaluated

- The VAS Fund introduces limits for some risks (stop loss), and these are fully transferred to the Fund of the Plan (already fully guaranteed by two hospitals), while extreme risks are excluded from the Fund of the Plan and they are transferred to the health insurance company.

- In practice it works in a way that capitation is increased by 30%, while 35% is levied by the doctors as withholdings. These resources can be accessed only by achieving savings.

- Savings are calculated in a way that costs evaluated according to their risks of the group of insured of the Plan MEDIPARTNER adjusted for extreme costs are compared with the costs of the reference group of insured from the same region (so called costs in the region)

Bibliography

- www.medipartner.sk

- Presentation materials of the Klient PRO SK and Dôvera health insurance company for the Plan MEDIPARTNER

Disclaimer: Peter Pažitný, Tomáš Szalay, Angelika Szalayová and Tomáš Macháček are owners of Klient PRO SK, which administers the Plan MEDIPARTNER in a partnership with the Dôvera Health Insurance Company.